AMP has upped their term deposit rates over a range of timeframes. At the time of posting these are the highest advertised rates on offer for interest paid annually.

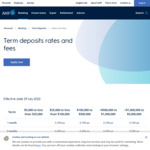

Highlights are for deposits over $25,000 up to $5 Million.

| Term | Interest rate |

|---|---|

| 1 year | 3.50% pa |

| 2 years | 3.90% pa |

| 3 years | 4.15% pa |

| 4 years | 4.30% pa |

| 5 years | 4.40% pa |

If you want to park some of your spare money, this is an interest-ing option, pun intended.

I am interested in these interesting interests but I don't have $25K so I am not interested.