I guess it’s the financial gift that keeps giving from Scotty from marketing that we’ll all end up paying for.

Tough times are afoot. How much do you think interest rates will go up today?

I guess it’s the financial gift that keeps giving from Scotty from marketing that we’ll all end up paying for.

Tough times are afoot. How much do you think interest rates will go up today?

I saw the 3% and laughed. They should have got no votes at all. But I am sure some people were gullible to turn up with iTunes gift cards and put it in the ballot box with their votes.

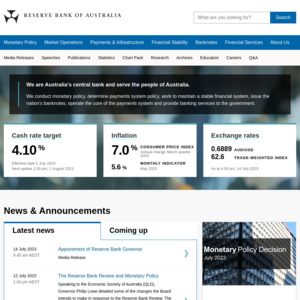

0.50bp rise

noice

Time for weak 🙌 to damp stonks.

asx is already damping

👍.

Time for ETFs to bleed.

0.5% Excellent.

50points biggest jump ive seen in my life time…. not saying it wasnt expected but it wont be good for consumer confidence.

wonder how it will go from here as the RBA has got the Cash rate back to pre-pandemic levels

there was no virus, ukraine war or 2 year shutdown then, rates are going one way and north

there was no virus, ukraine war or 2 year shutdown then, rates are going one way and north

Rates were still dropping prior to all those things…

RBA #1 target is a headline inflation rate of 2-3%. That's the defining policy of their operations and governance and will remain that way independently of the political powers in charge.

Until that rate falls into (or near) that target range, I wouldn't expect any cooling in the rate increases. Repetitive +50bps increases, unlikely, but once they reach a round quarter percent (i.e. 1.00/1.25), I'd expect repeated 25bps increases until they're happy with inflation.

Honestly quite surprised with the 50, and was personally expecting the 40 to bring them inline with their typical quarter increment rate, but with inflation rates as high as they are, I think their hand was forced to go as high as what the market would reasonably accept.

A nuance is that it targets inflation in line with its mission: "Stability of the Currency. Maintenance of Full Employment. Ensuring the economic prosperity of the welfare of the people of the Australia." So in principle, unlike the former Bundesbank, which did primarily target inflation, it could chose to pump housing to create a wealth effect, were it to believe it benefitted its mission. As such, it's potentially able to tolerate a lot more inflation, so long as these other goals are met. So as a general rule let's consider that if supply push inflation persists, it may not drag us into recession (though it may not have the choice anyway if we enter a global recession)

above most bank economist expectations but kind of in-line with market views.

With most loan approvals being based on a 2.5% (now 3%) interest buffer, the speed in which the market expects to see circa-3% central bank rate (mid-late 2023) will mean that a vast majority of loans issued in the last 5 years (particularly the last 2.5) will be hitting that threshold of bank loan affordability (the benchmark is that 30-40% of combined income used to service a loan).

People struggling to afford repayments now are more of an outlier, and are usually either experiencing a loss of income event or otherwise have very little control of their spending.

It is foreseeable however that come 2024, there may be several hundreds of thousands of households (particularly in urban fringes) that despite having 1-2 FT incomes and maintaining their typical income and expense habits, will not be able to meet with the repayments of their loan (refinancing will be difficult in a falling market) and may need to sell up or otherwise take a drastic cut to their quality of living to survive.

Not trying to be depressing but the state of our education curriculum (particularly in regards to personal financial management), and a lack of cultural awareness among the larger populous towards savvy, prudent spending, is a large reason why I see people complaining all the time. Ofc there are people in power influencing economic policy to keep prices buoyant, but I know too many people who go into property with a lack of understanding or control of their life (both personally and financially), and simply make emotional decisions (mainly to keep up appearances/ show off to friends), are are likely to regret it soon.

Next thing will be pressure on Albo to give an emergency "interest rate shock" handout.

Thats after the power shock handout which will happen soon.

Same old story. People spend ,spend spend on everything then bleat when reality strikes.

Just waitning for someone to post it's all the Baby Boomers fault.

yeah that aint happening, more handouts will just push the interest rates even higher.

Agree no way should it happen

Just saying there will be pressure going on from the over indebted splurging whingers.

@IanC: lol wait, you two lads saw Labor's stimulus package during the GFC (which handed Australia the #1 performing economy ON EARTH) as handing out candy?

@ThithLord: No,not at all.

There is a slight difference this time around.

I seem to recall that the credit card bill was then around $200 billion then NOT over 1 trillion as it is now ( very happy to be corrected)

That I think is 800 Billion more.

Just stating IMHO that the whinging overspendsers should not be propped up every time.

The next thing will be a breeders bonus.

@IanC: Righto, Righto, my mistake.

They racked up around $800B onto that original debt, and 2/3s of that debt was before COVID. Just FYI.

yep exactly. It'll be a shock to me if they do it, and likely just push inflation further. From what I've read though, it seems that Albo does construvely take on the words of the Department of Treasury (instead of side-lining them like ScoMo) and hopefully will listen to reasonable economic advice.

I'm in my early 20's and whilst I have a great understanding of this due to my work and education, so many of my friends (who are highly educated degree holders in technical fields) have literally no understanding of anything personal finance related (some don't even know how the tax system work, and yet completed years of under/post grad math/science). Its such an important aspect of life to know about, yet they'd likely know about the odds on Sportsbet than the interest rate.

Mind you, they all end up relatively well paid jobs for 23-25 yr olds (circa 80-100k) right out of uni, and 2 years down the track, they still think that buying a home (whilst still living at home) is a lifelong unobtainable dream. Most have no more than a few grand in savings (maybe 20-25k at most) and get instantly jealous when they hear of some friends (i.e. me) actively house hunting or getting into the market and expect gov intervention so that they can have immediate gratification (but don't want to make any sacrifices to their spending/ take on odd jobs to do so)

many of my friends (who are highly educated degree holders in technical fields) have literally no understanding of anything personal finance related (some don't even know how the tax system work, and yet completed years of under/post grad math/science).

Very good followers into professions but not very good at understanding anything else. These people actually keep the world moving.

Imagine if all of us are financially astute. How is scammers going to get us to pay our taxes in gift cards.

80-100k and living at home but only 20-25k savings? Did they buy a luxury car (lol)?

@Fobsessive: Yeah a lot of that.

Obviously not everyone did all these things, but I'm compiling what I've seen;

Going out at every opportunity for a night out/festivals (outside lockdowns), eating out 3-4 days a week (and at an insta worthy fancy restaurant at least once a week), buying nice new cars (or newish big rig 4wds) and more recently quite a bit on travel (if done well then I'm fully supportive of this).

Not to mention clothes/shoes (mainly the women, but quite a number of guys too), which was quite a big expense for a few during lockdown, alongside the typical daily ubereats.

Sportsbet was a big expense for a few too lol. Some made big $$$ though.

Not trying to be depressing but the state of our education curriculum (particularly in regards to personal financial management), and a lack of cultural awareness among the larger populous towards savvy, prudent spending, is a large reason why I see people complaining all the time.

Holding back is hard. It is like someone said if you could save $1k a month into the stock market index for 40 years you'll have like $2m. It is very hard for people to delay gratification. It feels like a prison sentence. It is much better being a prisoner to marketing from consumer goods companies.

Both very sound responses and I have to agree with you in them. I just find it puzzling that when arguably the smartest (educationally) in society aren’t able to comprehend their finances and thus fail to work their way up, what it means for the broader majority of society. Sad part is it’s my generation and the ones after who’ll likely campaign for some wealth tax that’ll further work to prop up the expeditious ways and penalise those like me who just want to make their money go further

I just find it puzzling that when arguably the smartest (educationally) in society aren’t able to comprehend their finances and thus fail to work their way up, what it means for the broader majority of society

Smartest believe they are smarter than everyone else. They can spend it and make more. Story of tortoise and the hare right? The poor person through disciplined savings could retire with more cash than a smart educated person. Because they have $2m in cash ($500k home) and live off $50k a year but the smart person has $1m cash (and a $2m house) and want a $100k lifestyle. Assuming both don't want to sell their cherished homes.

Most immigrant families the parents don't mind slaving away so their kids can get an education and a better life (so they can take care of them in their old age). Where as the born here and poor would like to be given what they are entitled to (house, car, education and money).

@netjock: that's a great response there and a very good way of putting it.

the 'poor' person mimics the story of my parents and being immigrant parents they've done exactly what you've said. Whilst financially they need no help (I do give them valuable free advice/tax minimisation strategies), I'll be around to help them in any way they need.

It is foreseeable however that come 2024, there may be several hundreds of thousands of households (particularly in urban fringes) that despite having 1-2 FT incomes and maintaining their typical income and expense habits, will not be able to meet with the repayments of their loan (refinancing will be difficult in a falling market) and may need to sell up or otherwise take a drastic cut to their quality of living to survive.

Don't you think if RBA keeps going at the current pace, the market will hit the bottom much sooner (let's say by early 2023) and RBA may start cutting rates again if we hit the peak of inflation or have a better control over it? It means that the reversal of downward cycle would be triggered much sooner than 2024. Add to it, economy of the US doesn't look to be in a great shape so fed may also go much less aggressively about increasing rates in the near future. It means the pressure on RBA to increase rates will be reduced to some extent, at least.

Like the childless couple in News.com.au this morning who are worried about interest rate rises after having their first home built that is 4 bed 3 bath double garage and who knows how many family rooms, butlers pantries and expensive finishes it has. No one has a starter home anymore. Can’t brag about your dream home if you can’t afford to live in it.

How much interest would term deposits be increased ?

what ever they feel like, hopefully .4 to .5 but i doubt it.

only AMP and Macq have decent rates.

im about to put some in those ones after july, higher rate than my fixed mortgage after tax

dont get locked into any term deposits yet, im waiting on the sidelines until after july

after july rate rise ill lock in for 12 delays income to next FY

What do you mean by '12 delays income to next FY'? Do you mind explaining?

@virhlpool: Lock it in for for twelve months, on July 4th delays income to the next financial year as pays out when it matures on july 4th 2023

Idiots - "now we can get into the property market because house prices will fall!"

Cost of living and inflation - "hold my beer".

Idiots - "now we can get into the property market because house prices will fall!"

And the monthly payments are still at the same unaffordable levels. Banks tighten lending criteria. I'm waiting for the articles where people have 30% deposit and the bank still doesn't want to lend because they can't pay the monthly repayments.

To all those people that bought overpriced million dollar homes in Sydney recently… ha ha ha ha ha ha ha

And everywhere else

Regions, Perth and Brisbane still growing. It’s just Sydney and Melbourne that reached peak of the cycle.

Also - watch rents going to the moon. These extra costs will go straight to the renters.

Don't worry.

They will damp stonks and ETFs before they sell their homes.

But what if they already sold off their stonks and ETFs for the deposit?

And the idiots libs wanted to let them get at their super as well.

@dust: I don't need to imagine, I can already retire if I want. I just choose not too because I like my job and I'm well paid.

@techlead: I suppose username checks out lol. Tech salaries have been going through the roof the past few years!

@dust: I feel sorry for the people doing it tough. Genuinely feel for those people who can't work from home. They've been affected so much by Covid. Teachers, nurses, delivery drivers etc etc, very sad.

@techlead: Hope the ATO do not come looking because there are huge penalties for just that sort of thing.

@IanC: As long as its in your investment strategy declaration, it is fine. How is it different to someone using their SMSF to buy an investment property? That's not diversified at all.

I've had advice from accountants and lawyers, its all above board. Plus its my own money. I'm only managing my own super, I'm not running a fund for anyone else.

@techlead: Anyone buying an investment property as a single asset in an SMSF not only irresponsible but also stupid.

As for the advice from accountants etc lol… you are ultimately responsible.

Good luck

@IanC: Of course, its my money. Its not illegal though and ATO will not penalize me. I'm not going to sue myself for losing money. Not that you can sue a trustee just for losing money anyway

@techlead: No problem as you are obviously a single trustee fund but wonder why not corporate trustee structure?

Would be the first thing any decent accountant or lawyer would suggest.

@IanC: I do have a corporate trustee structure.

I'm the sole shareholder and director of the corporate trustee which controls my SMSF. As I only have my own money in there, I can be a sole shareholder and director. If there's more than one beneficiary then there needs to be at least 2.

@IanC: Let's see what the Fed cooks up.

I've got buy orders ready. All the way down to $2000 USD for BTC. Let's go, I'm ready.

@IanC: Haven't thought about it yet. It would be a long long time before I can even touch my super. I'm very sure I'd be long retired by the time I'm 65, I reckon at least retired for 20 years by the time I'm 65.

The plan is not going to look for another job ever again. When I'm sick of this one, hopefully I'd have a passion project or something to keep me busy. That's what is keeping me from retiring right now, I want something to keep me busy, don't want to get bored. I know from my uni days, computers games cannot sustain me. If I played games all day, I'd be sick of it after a week.

@IanC: Hodl till the end, that's my exit strategy.

I've already got enough to be very comfortable. Even if all cryptos go to $0, I'd be fine.

Plus it's my own money.

It's not the user's 💵 unless they hodl the 🔑 or cash out.

Pension funds are the biggest Ponzi ever created where users 💵 are 🔒 away for 40Y.

It's a slow rug pull where the first in cash out and the last in is left holding the bag.

People who don't have risk management will hodl red until they vomit before they sell.

@cashless: I don't know about other people but I like to buy assets when they're in the dumpster.

The stonks market crashing and the real estate market crashing will lead weak 🙌 to sell the most risky assets first.

Have a guess as to what I'll be buying when that happens?

Have a guess as to what I'll be buying when that happens?

Crypto

I don't know about other people but I like to buy assets when they're in the dumpster.

Your crypto's been in the dumpster for a long time. You stopped talking about your neat crypto tricks.

Stop talking, it will do you some good.

@netjock: You sound 😩. Are your 🎒 bleeding?

I'm waiting for the stonks market to rage quit so that I can buy more at sub $25,000.

I can guarantee that Rekt knows way more than most.

Like most guarantees on the internet. Not worth anything.

you have no idea what you are talking about as always.

Neither do you. No clue what's about to hit the economy in next 12-24 months 🤣

No clue what's about to hit the economy in next 12-24 months 🤣

You have no idea what is going to hit crypto in the next 12 - 24 months. All you guys are just talking out of theory. Every theory behind crypto as inflation hedge and whatever else is pretty much proven not true so far. Even Plan B's model has broken down, he needs to find a new line to plot.

Crypto crowd believe they know something but if everything is just TA and drawing lines from historical price action forwards into the future then it means you don't know much about the future, just what happened in the past.

@netjock: Plan B is very old news. Nobody can predict where the market goes.

It's like chess. You just make educated probable guesses, that it's more likely to go one way and not the other, based on one's understanding of TA & FA & indicators etc. You can try "forecast" next few moves, but that's it.

That's why people who price predict X will go to $100k or $20k has no clue and no control. If you are certain, place a trade, set profit targets and stop loss. If you're unsure, you sit out. That's it. Nobody has 100% hit rate.

economy in next 12-24 months

btw I'm talking global economics, not cypto

It's like chess. You just make educated probable guesses

Chess is about as certain as you can get. If you are taking probable guesses then you haven't read the game instructions or read any books if you are serious about it.

btw I'm talking global economics

Maybe you should figure out crypto first and then have a crack at economics.

Cathie Wood tried to predict the bitcoin price. Unfortunately if she correctly predicted the performance of her investment funds would have been better.

Chess is about as certain as you can get.

Ever heard of blunders? Or maybe something outside your control affected things. Every move is a guess, no way of knowing what happens next.

crypto first and then have a crack at economics.

Porque no los dos?

Cathie Wood tried to predict the bitcoin price.

Impossible to predict.

@netjock: The 🧂 comes out when the 🎒 gets heavy.

I've seen enough 🐻 markets to recognise when people are underwater. They get 😡 and blame strangers saying that they don't know what they're talking about.

They kick themselves and 😭 before 🛌 for not selling sooner. They could sell now at a loss but that would 👊 their ego for fk up the 🎒.

They're 😱 to tell their partner that their 🎒 are hemorrhaging and that it may take years to recover from the 💉 🛀.

Stonks, ETFs and pension funds had a good 2Y run but now is the time to pay it ⬅️.

@rektrading: ^It's sad but it's sooo true. 🩸 in the streets

“Every man has two lives, and the second starts when he realizes he has just one” — Confucius.

@netjock: Define, "a long time". I saw some of my trade confirmations around two years back (mid June 2020) for under $300AU ETH. You don't need me to tell you how much ETH is worth today. :D

I don't understand why people can stomach losses for 5 or more years in property, yet for crypto, they need to instantly make millions or else its a scam. You do realise that when you purchase an investment property, you are instantly down the amount of stamp duty at least (because there are other costs too). So for the market to move so you are in the green, it usually takes years even during a bull market.

I look back at my trades just 2 years ago, all of them are up by multiples. Eg ETH 9x from June 2020. Has property prices 9x'd since 2020?

my trades just 2 years ago, all of them are up by multiples. Eg ETH 9x from June 2020. Has property prices 9x'd since 2020?

Just pick a point to start and pick a point at the end and disclose your profitable trades to show how good you are.

You could have bought CSL for $34 a share in 2012 and it would have 10x if you look at Feb 2020. I can give you trade confirmations too.

I don't understand why people can stomach losses for 5 or more years in property, yet for crypto, they need to instantly make millions or else its a scam.

You are not very good if you are comparing 5yrs with instant.

Apparently Clive Palmer has power over the rate as he was going to cap it.