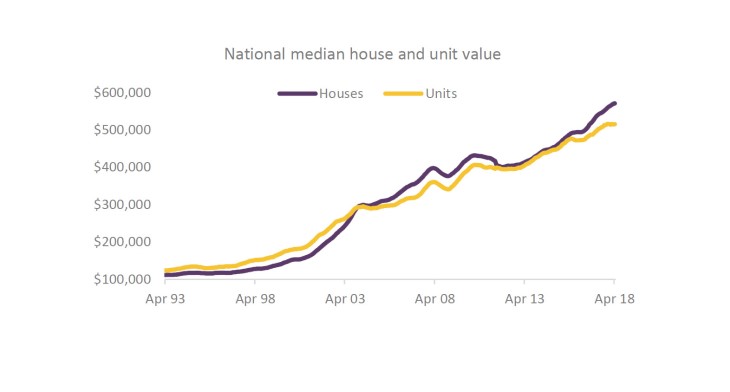

I am finding it hard to decide if it is wise to buy a property in the current FOMO fueled market or if its better to wait for things to settle down a bit. Its hard to tell if we are in a short term peak or the start of the next leg up.

It might be interesting to do a poll and look back on it at the end of this year to see if OzBargainers got it right.

{kind=link}

Buy now or pay more later.