Thanks JackOfSpade

Note that this account is currently paying only 0.85%

It says it will change on 1 April to add a savings bonus rate and that the total will be 1.25% (provided they don't change this variable rate before then, which they can because it's a variable rate)

cudos to the volunteers working on this spreadsheet

AMP says it will be back at 2nd place; higher than UBank. (ING is 1st but now has the grow every month requirement)

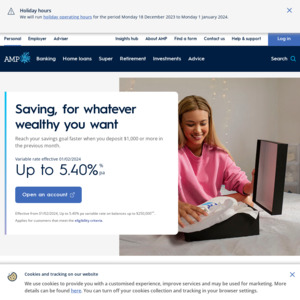

It looks like all you have to do is deposit $250 a month, to be eligible for the bonus rate in the next month.

Bonus paid on balances up to $250,000.

No monthly fee this time

No 5 transactions a month requirement.

No restrictions on withdrawals.

Opening this up as a place holder for discussions etc

Quick reminders about problems with previous products they had / I think this account doesn't have any of these problems at the moment

- one had a monthly fee that was waived if you met the bonus criteria (aka if you missed the deposit, they didn't pay bonus interest AND they penalized you)

- AMP Bett3r had 3 different bank accounts (ie PITA), and initially had confustion about where your deposit had to go to be eligible for the bonus

- one later added that you had to have a superannuation account with AMP and make regular contributions to that

Note: Darjimick says if you are between 18-29 there is an account where you can get 3%